14 Time Series Analysis

Introduction

Time series analysis has become a hot topic with the rise of quantitative finance and automated trading of securities. Many of the facilities described in this chapter were invented by practitioners and researchers in finance, securities trading, and portfolio management.

Before you start any time series analysis in R, a key decision is your choice of data representation (object class). This is especially critical in an object-oriented language such as R, because the choice affects more than how the data is stored; it also dictates which functions (methods) will be available for loading, processing, analyzing, printing, and plotting your data. When many people start using R they simply store time series data in vectors. That seems natural. However, they quickly discover that none of the coolest analytics for time series analysis work with simple vectors. We’ve found when users switch to using an object class intended for time series data, the analysis gets easier, opening a gateway to valuable functions and analytics.

This chapter’s first recipe recommends using the zoo or xts packages

for representing time series data. They are quite general and should

meet the needs of most users. Nearly every subsequent recipe assumes you

are using one of those two representations.

Note

The

xtsimplementation is a superset ofzoo, soxtscan do everything thatzoocan do. In this chapter, whenever a recipe works for azooobject, you can safely assume (unless stated otherwise) that it also works for anxtsobject.

Other Representations

Other representations of time series data are available in the R universe, including:

ftspackageirtsfrom thetseriespackagetimeSeriespackagets(base distribution)tsibblepackage, a tidyverse style package for time series

In fact, there is a whole toolkit, called tsbox, just for converting between representations.

Two representations deserve special mention.

ts (base distribution)

The base distribution of R includes a time series class called ts. We

don’t recommend this representation for general use because the

implementation itself is too limited and restrictive.

However, the base distribution includes some important time series analytics

that depend upon ts, such as the autocorrelation function (acf)

and the cross-correlation function (ccf).

To use those base functions on xts data, use the to.ts function

to “downshift” your data into the ts representation before calling the function.

For example, if x is an xts object, you can compute its autocorrelation

like this:

acf(as.ts(x))tsibble package

The tsibble package is a recent extension to the tidyverse,

specifically designed for working with time series data

within the tidyverse.

We find it useful for cross-sectional data—that is, data for which the observations are grouped by date,

and you want to perform analytics within dates more

than across dates.

Date Versus Datetime

Every observation in a time series has an associated date or time. The

object classes used in this chapter, zoo and xts, give you the

choice of using either dates or datetimes for representing the data’s

time component. You would use dates to represent daily data, of course,

and also for weekly, monthly, or even annual data; in these cases, the

date gives the day on which the observation occurred. You would use

datetimes for intraday data, where both the date and time of observation

are needed.

In describing this chapter’s recipes, we found it pretty cumbersome to keep saying “date or datetime.” So we simplified the prose by assuming that your data are daily and thus use whole dates. Please bear in mind, of course, that you are free and able to use timestamps below the resolution of a calendar date.

See Also

R has many useful functions and packages for time series analysis. You’ll find pointers to them in the task view for Time Series Analysis.

14.1 Representing Time Series Data

Problem

You want an R data structure that can represent time series data.

Solution

We recommend the zoo and xts packages. They define a data structure

for time series, and they contain many useful functions for working with

time series data. Create a zoo object this way where x is a vector, matrix,

or data frame, and dt is a vector of corresponding dates or datetimes:

Create an xts object in this way:

Convert between representations of the time series data by using

as.zoo and as.xts:

as.zoo(ts)Converts

tsto azooobjectas.xts(ts)Converts

tsto anxtsobject

Discussion

R has at least eight different implementations of data structures for

representing time series. We haven’t tried them all, but we can say that zoo and xts are excellent packages for working with

time series data and better than the others that we have tried.

These representations assume you have two vectors: a vector of

observations (data) and a vector of dates or times of those

observations. The zoo function combines them into a zoo object:

library(zoo)

#>

#> Attaching package: 'zoo'

#> The following objects are masked from 'package:base':

#>

#> as.Date, as.Date.numeric

x <- c(3, 4, 1, 4, 8)

dt <- seq(as.Date("2018-01-01"), as.Date("2018-01-05"), by = "days")

ts <- zoo(x, dt)

print(ts)

#> 2018-01-01 2018-01-02 2018-01-03 2018-01-04 2018-01-05

#> 3 4 1 4 8The xts function is similar, returning an xts object:

library(xts)

#> Registered S3 method overwritten by 'xts':

#> method from

#> as.zoo.xts zoo

#>

#> Attaching package: 'xts'

#> The following objects are masked from 'package:dplyr':

#>

#> first, last

ts <- xts(x, dt)

print(ts)

#> [,1]

#> 2018-01-01 3

#> 2018-01-02 4

#> 2018-01-03 1

#> 2018-01-04 4

#> 2018-01-05 8The data, x, should be numeric. The vector of dates or datetimes,

dt, is called the index. Legal indices vary between the packages:

zooThe index can be any ordered values, such as

Dateobjects,POSIXctobjects, integers, or even floating-point values.xtsThe index must be a supported date or time class. This includes

Date,POSIXct, andchronobjects. Those should be sufficient for most applications, but you can also useyearmon,yearqtr, anddateTimeobjects. Thextspackage is more restrictive thanzoobecause it implements powerful operations that require a time-based index.

The following example creates a zoo object that contains the price of

IBM stock for the first five days of 2010; it uses Date objects for

the index:

prices <- c(132.45, 130.85, 130.00, 129.55, 130.85)

dates <- as.Date(c(

"2010-01-04", "2010-01-05", "2010-01-06",

"2010-01-07", "2010-01-08"

))

ibm.daily <- zoo(prices, dates)

print(ibm.daily)

#> 2010-01-04 2010-01-05 2010-01-06 2010-01-07 2010-01-08

#> 132 131 130 130 131In contrast, the next example captures the price of IBM stock at one-second intervals. It represents time by the number of hours past midnight starting at 9:30 a.m. (1 second = 0.00027778 hours, more or less):

prices <- c(131.18, 131.20, 131.17, 131.15, 131.17)

seconds <- c(9.5, 9.500278, 9.500556, 9.500833, 9.501111)

ibm.sec <- zoo(prices, seconds)

print(ibm.sec)

#> 10 10 10 10 10

#> 131 131 131 131 131Those two examples used a single time series, where the data came from a

vector. Both zoo and xts can also handle multiple, parallel time

series. For this, capture the several time series in a matrix or data frame and

then create a multivariate time series by calling the zoo (or xts)

function:

The second argument is a vector of dates (or datetimes) for each observation. There is only one vector of dates for all the time series; in other words, all observations in each row of the matrix or data frame must have the same date. See Recipe 14.5, “Merging Several Time Series” if your data has mismatched dates.

Once the data is captured inside a zoo or xts object, you can

extract the pure data via coredata, which returns a simple vector (or

matrix):

You can extract the date or time portion via index:

The xts package is very similar to zoo. It is optimized for

speed, so is especially well suited for processing large volumes of

data. It is also clever about converting to and from other time series

representations.

One big advantage of capturing data inside a zoo or xts object is

that special-purpose functions become available for printing, plotting,

differencing, merging, periodic sampling, applying rolling functions,

and other useful operations. There is even a function, read.zoo,

dedicated to reading time series data from ASCII files.

Remember that the xts package can do everything that the zoo package

can do, so everywhere that this chapter talks about zoo objects you

can also use xts objects.

If you are a serious user of time series data, we strongly recommend studying the documentation of these packages in order to learn about the ways they can improve your life. They are rich packages with many useful features.

See Also

See CRAN for documentation on

zoo and

xts, including reference manuals, vignettes, and quick reference cards. If the

packages are already installed on your computer, view their

documentation using the vignette function:

The timeSeries package is another good implementation of a time series

object. It is part of the Rmetrics project for quantitative finance.

14.2 Plotting Time Series Data

Problem

You want to plot one or more time series.

Solution

Use plot(x), which works for zoo objects and xts objects

containing either single or multiple time series.

For a simple vector v of time series observations, you can use either

plot(v,type = "l") or plot.ts(v).

Discussion

The generic plot function has a version for zoo objects and xts

objects. It can plot objects that contain a single time series or

multiple time series. In the latter case, it can plot each series in a

separate plot or together in one plot.

Suppose that ibm.infl is a zoo object that contains two time series.

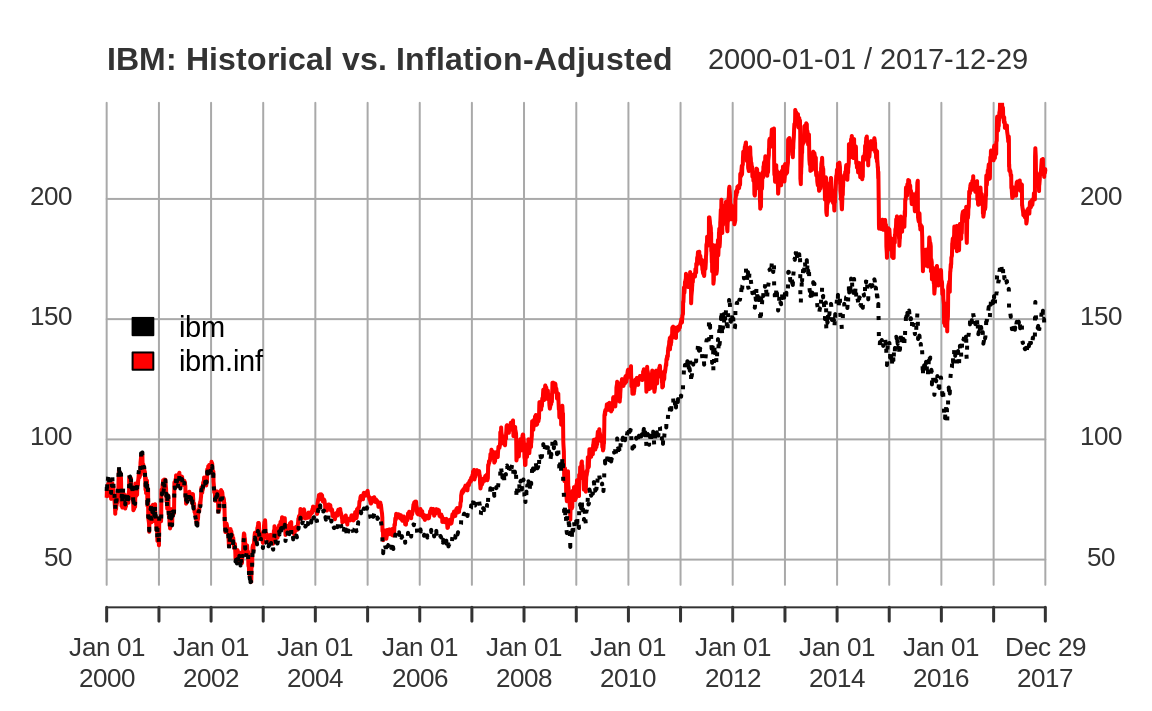

One shows the quoted price of IBM stock from January 2000 through December 2017, and the other is that same price adjusted for inflation. If you plot the object, R will plot the two time series together in one plot, as shown in Figure 14.1:

load(file = "./data/ibm.rdata")

library(xts)

main <- "IBM: Historical vs. Inflation-Adjusted"

lty <- c("dotted", "solid")

# Plot the xts object

plot(ibm.infl,

lty = lty, main = main,

legend.loc = "left"

)

Figure 14.1: Example xts plot

The plot function for xts provides a default title as simply the name of the xts object. As we show here, it’s common to set the main parameter to a more meaningful title.

The code specifies two line types (lty) so that the two lines are

drawn in two different styles, making them easier to distinguish.

See Also

For working with financial data, the quantmod package contains special

plotting functions that produce beautiful, stylized plots.

14.3 Extracting the Oldest or Newest Observations

Problem

You want to see only the oldest or newest observations of your time series.

Solution

Use head to view the oldest observations:

Use tail to view the newest observations:

Discussion

The head and tail functions are generic, so they will work whether

your data is stored in a simple vector, a zoo object, or an xts

object.

Suppose you have a xts object with a multiyear history of the price of

IBM stock like the one used in the prior recipe. You can’t display the whole dataset because it would scroll

off your screen. But you can view the initial observations:

ibm <- ibm.infl$ibm # grab one column for illustration

head(ibm)

#> ibm

#> 2000-01-01 78.6

#> 2000-01-03 82.0

#> 2000-01-04 79.2

#> 2000-01-05 82.0

#> 2000-01-06 80.6

#> 2000-01-07 80.2And you can view the final observations:

tail(ibm)

#> ibm

#> 2017-12-21 148

#> 2017-12-22 149

#> 2017-12-26 150

#> 2017-12-27 150

#> 2017-12-28 151

#> 2017-12-29 150By default, head and tail show (respectively) the six oldest and six

newest observations. You can see more observations by providing a second

argument—for example, tail(ibm, 20).

The xts package also includes first and last functions, which use

calendar periods instead of number of observations. We can use first

and last to select data by number of days, weeks, months, or even

years:

first(ibm, "2 week")

#> ibm

#> 2000-01-01 78.6

#> 2000-01-03 82.0

#> 2000-01-04 79.2

#> 2000-01-05 82.0

#> 2000-01-06 80.6

#> 2000-01-07 80.2At first glance this output might be confusing. We asked for "2 week" and xts returned six days. That might seem off until we look at a calendar of January 2000.

Figure 14.2: January 2000 calendar

We can see from the calendar that the first week of January 2000 has only one day, Saturday the 1st. Then the second week runs from the 2nd to the 8th. Our data has no value for the 8th, so when we ask first for the first "2 week" it returns all the values from the first two calendar weeks. In our example dataset the first two calendar weeks contain only six values.

Similarly, we can ask last to give us the last month’s worth of data:

last(ibm, "month")

#> ibm

#> 2017-12-01 152

#> 2017-12-04 153

#> 2017-12-05 152

#> 2017-12-06 151

#> 2017-12-07 150

#> 2017-12-08 152

#> 2017-12-11 152

#> 2017-12-12 154

#> 2017-12-13 151

#> 2017-12-14 151

#> 2017-12-15 149

#> 2017-12-18 150

#> 2017-12-19 150

#> 2017-12-20 150

#> 2017-12-21 148

#> 2017-12-22 149

#> 2017-12-26 150

#> 2017-12-27 150

#> 2017-12-28 151

#> 2017-12-29 150If we had been using zoo objects here, we would need to have converted them to xts objects before passing the objects to first or last, as those are xts functions.

See Also

See help(first.xts) and help(last.xts) for details on the first

and last functions, respectively.

Warning

The

tidyversepackagedplyralso has functions calledfirstandlast. If your workflow involves loading bothxtsanddplyrpackages, make sure to be explicit about which function you are calling by using the*package*::*function*notation (for example,xts::first).

14.4 Subsetting a Time Series

Problem

You want to select one or more elements from a time series.

Solution

You can index a zoo or xts object by position. Use one or two

subscripts, depending upon whether the object contains one time series

or multiple time series:

ts[i]Selects the ith observation from a single time series

ts[j,i]Selects the ith observation of the jth time series of multiple time series

You can index the time series by date. Use the same type of

object as the index of your time series. This example assumes that the

index contains Date objects:

You can index it by a sequence of dates:

The window function can select a range by start and end date:

Discussion

Recall our xts object that is a sample of inflation-adjusted IBM stock prices from the previous recipe:

head(ibm)

#> ibm

#> 2000-01-01 78.6

#> 2000-01-03 82.0

#> 2000-01-04 79.2

#> 2000-01-05 82.0

#> 2000-01-06 80.6

#> 2000-01-07 80.2We can select an observation by position, just like selecting elements from a vector (see Recipe 2.9, “Selecting Vector Elements”):

We can also select multiple observations by position:

Sometimes it’s more useful to select by date. Simpy use the date itself as the index.

Our ibm data is an xts object, so we can use date-like subsetting, too. (The zoo object does not offer this flexibility.)

ibm['2010-01-05']

ibm['20100105']We can also select by a vector of Date objects:

dates <- seq(as.Date("2010-01-04"), as.Date("2010-01-08"), by = 2)

ibm[dates]

#> ibm

#> 2010-01-04 104

#> 2010-01-06 102

#> 2010-01-08 103The window function is easier for selecting a range of consecutive

dates:

window(ibm, start = as.Date("2010-01-05"), end = as.Date("2010-01-07"))

#> ibm

#> 2010-01-05 103

#> 2010-01-06 102

#> 2010-01-07 102We can select a year/month combination using yyyymm subsetting:

Select year ranges using / like so:

Or use / to select ranges including months:

See Also

The xts package provides many other clever ways to index a time

series. See the package documentation.

14.5 Merging Several Time Series

Problem

You have two or more time series. You want to merge them into a single time series object.

Solution

Use a zoo or xts object to represent the time series, then use the merge

function to combine them:

Discussion

Merging two time series is an incredible headache when the two series have differing timestamps. Consider these two time series: the daily price of IBM stock from 1999 through 2017, and the monthly Consumer Price Index (CPI) for the same period:

load(file = "./data/ibm.rdata")

head(ibm)

#> ibm

#> 1999-01-04 64.2

#> 1999-01-05 66.5

#> 1999-01-06 66.2

#> 1999-01-07 66.7

#> 1999-01-08 65.8

#> 1999-01-11 66.4

head(cpi)

#> cpi

#> 1999-01-01 0.938

#> 1999-02-01 0.938

#> 1999-03-01 0.938

#> 1999-04-01 0.945

#> 1999-05-01 0.945

#> 1999-06-01 0.945Obviously, the two time series have different timestamps because one is daily data and the other is monthly data. Even worse, the downloaded CPI data is timestamped for the first day of every month, even when that day is a holiday or weekend (e.g., New Year’s Day).

Thank goodness for the merge function, which handles the messy details

of reconciling the different dates:

head(merge(ibm, cpi))

#> ibm cpi

#> 1999-01-01 NA 0.938

#> 1999-01-04 64.2 NA

#> 1999-01-05 66.5 NA

#> 1999-01-06 66.2 NA

#> 1999-01-07 66.7 NA

#> 1999-01-08 65.8 NABy default, merge finds the union of all dates: the output contains

all dates from both inputs, and missing observations are filled with NA

values. You can replace those NA values with the most recent observation

by using the na.locf function from the zoo package:

head(na.locf(merge(ibm, cpi)))

#> ibm cpi

#> 1999-01-01 NA 0.938

#> 1999-01-04 64.2 0.938

#> 1999-01-05 66.5 0.938

#> 1999-01-06 66.2 0.938

#> 1999-01-07 66.7 0.938

#> 1999-01-08 65.8 0.938(Here locf stands for “last observation carried forward.”) Observe

that the NAs were replaced. However, na.locf left an NA in the first

observation (1999-01-01) because there was no IBM stock price on that

day.

You can get the intersection of all dates by setting all = FALSE:

head(merge(ibm, cpi, all = FALSE))

#> ibm cpi

#> 1999-02-01 63.1 0.938

#> 1999-03-01 59.2 0.938

#> 1999-04-01 62.3 0.945

#> 1999-06-01 79.0 0.945

#> 1999-07-01 92.4 0.949

#> 1999-09-01 89.8 0.956Now the output is limited to observations that are common to both files.

Notice, however, that the intersection begins on February 1, not January 1. The reason is that January 1 is a holiday, so there is no IBM stock price for that date and hence no intersection with the CPI data. To fix this, see Recipe 14.6, “Filling or Padding a Time Series”.

14.6 Filling or Padding a Time Series

Problem

Your time series data is missing observations. You want to fill or pad the data with the missing dates/times.

Solution

Create a zero-width (dataless) zoo or xts object with the missing

dates/times. Then merge your data with the zero-width object, taking the

union of all dates:

Discussion

The zoo package includes a handy feature in the constructor for zoo

objects: you can omit the data and build a zero-width object. The object

contains no data, just dates. We can use these “Frankenstein” objects to

perform such operations as filling and padding on other time series

objects.

Suppose you download monthly CPI data used in the last recipe. The data is timestamped with the first day of each month:

head(cpi)

#> cpi

#> 1999-01-01 0.938

#> 1999-02-01 0.938

#> 1999-03-01 0.938

#> 1999-04-01 0.945

#> 1999-05-01 0.945

#> 1999-06-01 0.945As far as R knows, we have no observations for the other days of the months. However, we know that each CPI value applies to the subsequent days through month-end. So first we build a zero-width object with every day of the decade, but no data:

We use the min(index(cpi)) and max(index(cpi)) to get the minimum and maximum index value from our cpidata. So our resulting empty object is just an index of daily dates with the same range as our cpi data.

Then we take the union the CPI data and the zero-width object, yielding

a dataset filled with NA values:

filled.cpi <- merge(cpi, empty, all = TRUE)

head(filled.cpi)

#> cpi

#> 1999-01-01 0.938

#> 1999-01-02 NA

#> 1999-01-03 NA

#> 1999-01-04 NA

#> 1999-01-05 NA

#> 1999-01-06 NAThe resulting time series contains every calendar day, with NAs where

there was no observation. That might be what you need. However, a more

common requirement is to replace each NA with the most recent

observation as of that date. The na.locf function from the zoo

package does exactly that:

filled.cpi <- na.locf(merge(cpi, empty, all = TRUE))

head(filled.cpi)

#> cpi

#> 1999-01-01 0.938

#> 1999-01-02 0.938

#> 1999-01-03 0.938

#> 1999-01-04 0.938

#> 1999-01-05 0.938

#> 1999-01-06 0.938January’s value of 1 is carried forward until February 1, at which

time it is replaced by the February value. Now every day has the

latest CPI value as of that date. Note that in this dataset, the CPI is based on January 1, 1999 = 100% and all CPI values are relative to the value on that date.

tail(filled.cpi)

#> cpi

#> 2017-11-26 1.41

#> 2017-11-27 1.41

#> 2017-11-28 1.41

#> 2017-11-29 1.41

#> 2017-11-30 1.41

#> 2017-12-01 1.41We can use this recipe to fix the problem mentioned in Recipe 14.5, “Merging Several Time Series”. There, the daily price of

IBM stock and the monthly CPI data had no intersection on certain days.

We can fix that using several different methods. One way is to pad the

IBM data to include the CPI dates and then take the intersection (recall

that index(cpi) returns all the dates in the CPI time series):

filled.ibm <- na.locf(merge(ibm, zoo(, index(cpi))))

head(merge(filled.ibm, cpi, all = FALSE))

#> ibm cpi

#> 1999-01-01 NA 0.938

#> 1999-02-01 63.1 0.938

#> 1999-03-01 59.2 0.938

#> 1999-04-01 62.3 0.945

#> 1999-05-01 73.6 0.945

#> 1999-06-01 79.0 0.945That gives monthly observations. Another way is to fill out the CPI data (as described previously) and then take the intersection with the IBM data. That gives daily observations, as follows:

filled_data <- merge(ibm, filled.cpi, all = FALSE)

head(filled_data)

#> ibm cpi

#> 1999-01-04 64.2 0.938

#> 1999-01-05 66.5 0.938

#> 1999-01-06 66.2 0.938

#> 1999-01-07 66.7 0.938

#> 1999-01-08 65.8 0.938

#> 1999-01-11 66.4 0.938Another common method for filling missing values uses the cubic spline technique,

which interpolates smooth intermediate values from the known data.

We can use the zoo function na.spline to fill our missing values using a cubic spline.

combined_data <- merge(ibm, cpi, all = TRUE)

head(combined_data)

#> ibm cpi

#> 1999-01-01 NA 0.938

#> 1999-01-04 64.2 NA

#> 1999-01-05 66.5 NA

#> 1999-01-06 66.2 NA

#> 1999-01-07 66.7 NA

#> 1999-01-08 65.8 NA

combined_spline <- na.spline(combined_data)

head(combined_spline)

#> ibm cpi

#> 1999-01-01 4.59 0.938

#> 1999-01-04 64.19 0.938

#> 1999-01-05 66.52 0.938

#> 1999-01-06 66.21 0.938

#> 1999-01-07 66.71 0.938

#> 1999-01-08 65.79 0.938Notice that both the missing values for cpi and ibm were filled. However, the value filled in for January 1, 1999 for the ibm column seems out of line with the January 4th observation. This illustrates one of the challenges with cubic splines: they can become quite unstable if the value that is being interpolated is at the very beginning or the very end of a series. To get around this instability, we could get some data points from before January 1st, 1999, then interpolate using na.spline, or we could simply choose a different interpolation method.

14.7 Lagging a Time Series

Problem

You want to shift a time series in time, either forward or backward.

Solution

Use the lag function. The second argument, k, is the number of periods

to shift the data:

Use positive k to shift the data forward in time (tomorrow’s data

becomes today’s data). Use a negative k to shift the data backward in

time (yesterday’s data becomes today’s data).

Discussion

Recall the zoo object containing five days of IBM stock prices from Recipe 14.1, “Representing Time Series Data”:

To shift the data forward one day, we use k = +1:

lag(ibm.daily, k = +1, na.pad = TRUE)

#> 2010-01-04 2010-01-05 2010-01-06 2010-01-07 2010-01-08

#> NA 132 131 130 130We also set na.pad = TRUE to fill the trailing dates with NA. Otherwise,

they would simply be dropped, resulting in a shortened time series.

To shift the data backward one day, we use k = -1. Again we use

na.pad = TRUE to pad the beginning with NAs:

lag(ibm.daily, k = -1, na.pad = TRUE)

#> 2010-01-04 2010-01-05 2010-01-06 2010-01-07 2010-01-08

#> NA 132 131 130 130If the sign convention for k seems odd to you, you are not alone.

Warning

The function is called

lag, but a positivekactually generates leading data, not lagging data. Use a negativekto get lagging data. Yes, this is bizarre. Perhaps the function should have been calledlead.

The other thing to be careful with when using lag is that the dplyr package contains a function named lag as well. The arguments for dplyr::lag are not exactly the same as the Base R lag function. In particular, dplyr uses n instead of k:

dplyr::lag(ibm.daily, n = 1)

#> 2010-01-04 2010-01-05 2010-01-06 2010-01-07 2010-01-08

#> NA 132 131 130 130Warning

If you want to load

dplyr, you should use the namespace to be explicit about whichlagfunction you are using. The Base R function isstats::lag, while the dplyr function is, naturally,dplyr::lag.

14.8 Computing Successive Differences

Problem

Given a time series, x, you want to compute the difference between successive observations: (x2 – x1), (x3 – x2), (x4 – x3), ….

Discussion

The diff function is generic, so it works on simple vectors, xts objects, and

zoo objects. The beauty of differencing a zoo or xts object is that the

result is the same type object you started with and the differences have the correct

dates. Here we compute the differences for successive prices of IBM

stock:

ibm.daily

#> 2010-01-04 2010-01-05 2010-01-06 2010-01-07 2010-01-08

#> 132 131 130 130 131

diff(ibm.daily)

#> 2010-01-05 2010-01-06 2010-01-07 2010-01-08

#> -1.60 -0.85 -0.45 1.30The difference labeled 2010-01-05 is the change from the previous day (2010-01-04), which is usually what you want. The differenced series is shorter than the original series by one element because R can’t compute the change as of 2010-01-04, of course.

By default, diff computes successive differences. You can compute

differences that are more widely spaced by using its lag parameter.

Suppose you have monthly CPI data and want to compute the change from

the previous 12 months, giving the year-over-year change. Specify a lag

of 12:

head(cpi, 24)

#> cpi

#> 1999-01-01 0.938

#> 1999-02-01 0.938

#> 1999-03-01 0.938

#> 1999-04-01 0.945

#> 1999-05-01 0.945

#> 1999-06-01 0.945

#> 1999-07-01 0.949

#> 1999-08-01 0.952

#> 1999-09-01 0.956

#> 1999-10-01 0.957

#> 1999-11-01 0.959

#> 1999-12-01 0.961

#> 2000-01-01 0.964

#> 2000-02-01 0.968

#> 2000-03-01 0.974

#> 2000-04-01 0.973

#> 2000-05-01 0.975

#> 2000-06-01 0.981

#> 2000-07-01 0.983

#> 2000-08-01 0.983

#> 2000-09-01 0.989

#> 2000-10-01 0.990

#> 2000-11-01 0.992

#> 2000-12-01 0.994

head(diff(cpi, lag = 12), 24) # Compute year-over-year change

#> cpi

#> 1999-01-01 NA

#> 1999-02-01 NA

#> 1999-03-01 NA

#> 1999-04-01 NA

#> 1999-05-01 NA

#> 1999-06-01 NA

#> 1999-07-01 NA

#> 1999-08-01 NA

#> 1999-09-01 NA

#> 1999-10-01 NA

#> 1999-11-01 NA

#> 1999-12-01 NA

#> 2000-01-01 0.0262

#> 2000-02-01 0.0302

#> 2000-03-01 0.0353

#> 2000-04-01 0.0285

#> 2000-05-01 0.0296

#> 2000-06-01 0.0353

#> 2000-07-01 0.0342

#> 2000-08-01 0.0319

#> 2000-09-01 0.0330

#> 2000-10-01 0.0330

#> 2000-11-01 0.0330

#> 2000-12-01 0.033014.9 Performing Calculations on Time Series

Problem

You want to use arithmetic and common functions on time series data.

Solution

No problem. R is pretty clever about operations on zoo and xts objects. You

can use arithmetic operators (+, -, *, /, etc.) as well as

common functions (sqrt, log, etc.) and usually get what you

expect.

Discussion

When you perform arithmetic on zoo or xts objects, R aligns the objects

according to date so that the results make sense. Suppose we want to

compute the percentage change in IBM stock. We need to divide the daily

change by the price, but those two time series are not naturally

aligned—they have different start times and different lengths. Here’s an illustration with a zoo object:

ibm.daily

#> 2010-01-04 2010-01-05 2010-01-06 2010-01-07 2010-01-08

#> 132 131 130 130 131

diff(ibm.daily)

#> 2010-01-05 2010-01-06 2010-01-07 2010-01-08

#> -1.60 -0.85 -0.45 1.30Fortunately, when we divide one series by the other, R aligns the series

for us and returns a zoo object:

diff(ibm.daily) / ibm.daily

#> 2010-01-05 2010-01-06 2010-01-07 2010-01-08

#> -0.01223 -0.00654 -0.00347 0.00994We can scale the result by 100 to compute the percentage change, and the

result is another zoo object:

100 * (diff(ibm.daily) / ibm.daily)

#> 2010-01-05 2010-01-06 2010-01-07 2010-01-08

#> -1.223 -0.654 -0.347 0.994Functions work just as well. If we compute the logarithm or square root

of a zoo object, the result is a zoo object with the timestamps

preserved:

log(ibm.daily)

#> 2010-01-04 2010-01-05 2010-01-06 2010-01-07 2010-01-08

#> 4.89 4.87 4.87 4.86 4.87In investment management, computing the difference of logarithms of prices is quite common. That’s a piece of cake in R:

See Also

See Recipe 14.8, “Computing Successive Differences”, for the special case of computing the difference between successive values.

14.10 Computing a Moving Average

Problem

You want to compute the moving average of a time series.

Solution

Use the rollmean function of the zoo package to calculate the

k-period moving average:

Here ts is the time series data, captured in a zoo object, and k is

the number of periods.

For most financial applications, you want rollmean to calculate the

mean using only historical data; that is, for each day, use only the

data available that day. To do that, specify align = right. Otherwise,

rollmean will “cheat” and use future data that was actually

unavailable at the time:

Discussion

Traders are fond of moving averages for smoothing out fluctuations in

prices. The formal name is the rolling mean. You could calculate the

rolling mean as described in Recipe 14.12, “Applying a Rolling Function”, by combining the

rollapply function and the mean function, but rollmean is much

faster.

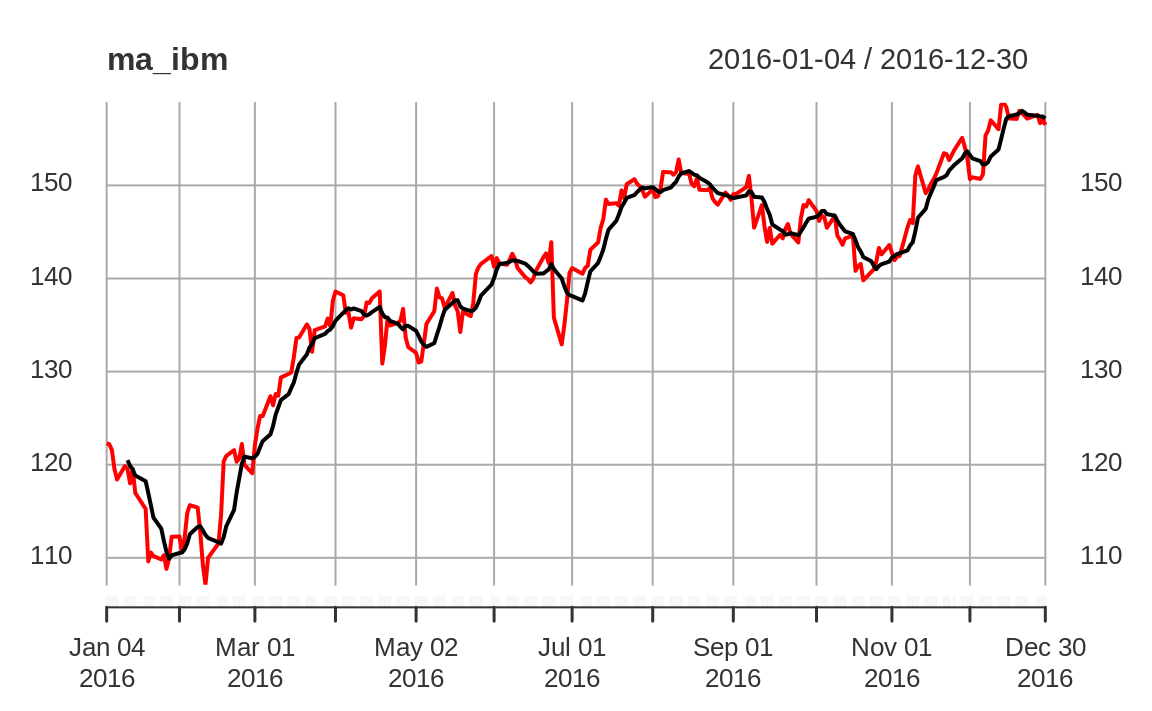

Beside speed, the beauty of rollmean is that it returns the same type of time series object it’s called on (i.e., xts or zoo). For each element in the object, its date is the “as of” date for

a calculated mean. Because the result is a time series object, you can easily merge the

original data and the moving average and then plot them together as in Figure 14.3:

ibm_year <- ibm["2016"]

ma_ibm <- rollmean(ibm_year, 7, align = "right")

ma_ibm <- merge(ma_ibm, ibm_year)

plot(ma_ibm)

Figure 14.3: Rolling average plot

The output is normally missing a few initial data points, since

rollmean needs a full k observations to compute the mean.

Consequently, the output is shorter than the input. If that’s a problem,

specify na.pad = TRUE; then rollmean will pad the initial output with

NA values.

See Also

See Recipe 14.12, “Applying a Rolling Function”, for more about the

align parameter.

The moving average described here is a simple moving average. The

quantmod, TTR, and fTrading packages contain functions for

computing and plotting many kinds of moving averages, including simple

ones.

14.11 Applying a Function by Calendar Period

Problem

Given a time series, you want to group the contents by a calendar period (e.g., week, month, or year) and then apply a function to each group.

Solution

The xts package includes functions for processing a time series by

day, week, month, quarter, or year:

apply.daily(ts, f)

apply.weekly(ts, f)

apply.monthly(ts, f)

apply.quarterly(ts, f)

apply.yearly(ts, f)Here ts is an xts time series, and f is the function to apply to each

day, week, month, quarter, or year.

If your time series is a zoo object, convert to an xts object first

so you can access these functions; for example:

Discussion

It is common to process time series data according to calendar period. But figuring calendar periods is tedious at best and bizarre at worst. Let these functions do the heavy lifting.

Suppose we have a five-year history of IBM stock prices stored in an

xts object:

ibm_5 <- ibm["2012/2017"]

head(ibm_5)

#> ibm

#> 2012-01-03 152

#> 2012-01-04 151

#> 2012-01-05 150

#> 2012-01-06 149

#> 2012-01-09 148

#> 2012-01-10 148We can calculate the average price by month if we use apply.monthly

and mean together:

ibm_mm <- apply.monthly(ibm_5, mean)

head(ibm_mm)

#> ibm

#> 2012-01-31 151

#> 2012-02-29 158

#> 2012-03-30 166

#> 2012-04-30 167

#> 2012-05-31 164

#> 2012-06-29 159Notice that the IBM data is in an xts object from the start. Had the data been in a zoo object, we would have needed to convert it to xts using as.xts.

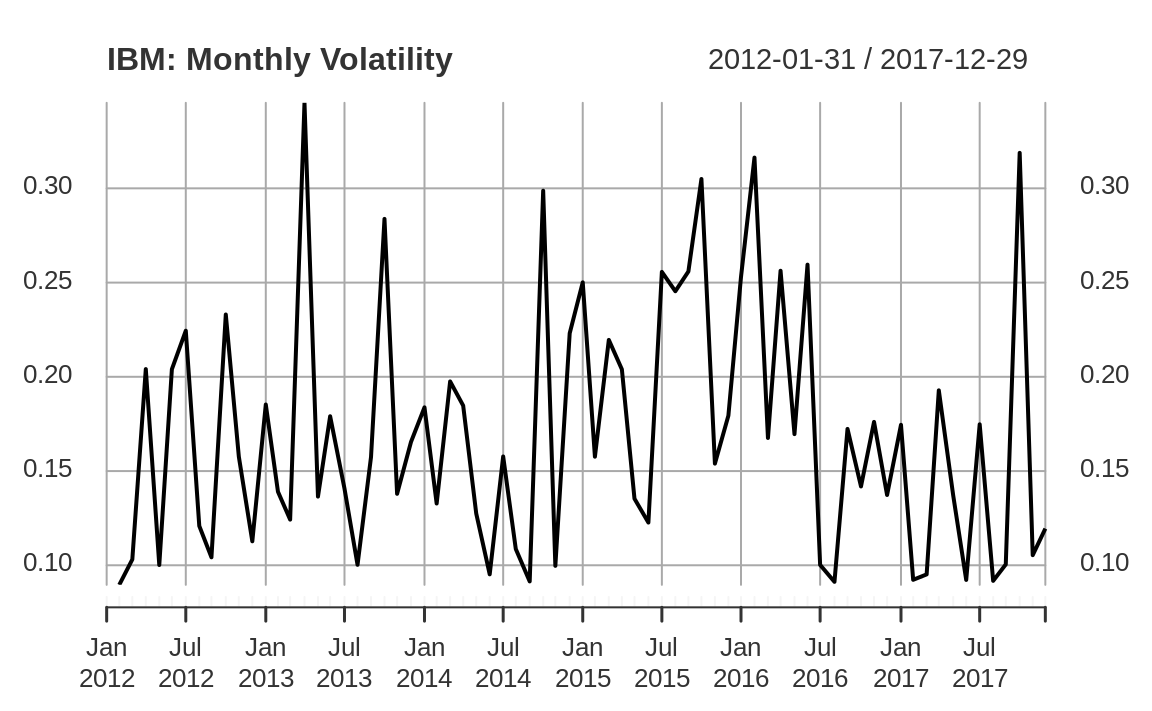

A more interesting application is calculating volatility by calendar month, where volatility is measured as the standard deviation of daily log-returns. Daily log-returns are calculated this way:

We calculate their standard deviation, month by month, like this:

We can scale the daily number to estimate annualized volatility, as shown in Figure 14.4:

ibm_vol <- sqrt(251) * apply.monthly(as.xts(diff(log(ibm_5))), sd)

plot(ibm_vol,

main = "IBM: Monthly Volatility"

)

Figure 14.4: IBM volatility plot

14.12 Applying a Rolling Function

Problem

You want to apply a function to a time series in a rolling manner: calculate the function at a data point using some window of time around that point, move to the next data point, calculate the function around that point, move to the next data point, and so forth.

Solution

Use the rollapply function in the zoo package. The width parameter

defines how many data points from the time series (ts) should be

processed by the function (f) at each point:

For many applications, you will likely set align = "right" to avoid

computing f with historical data that was unavailable at the time:

Discussion

The rollapply function extracts a “window” of data from your time

series, calls your function with that data, saves the result, and moves

to the next window—and repeats this pattern for the entire input. As an

illustration, consider calling rollapply with width = 21:

rollapply will repeatedly call the function, f, with a sliding

window of data, like this:

f(ts[1:21])f(ts[2:22])f(ts[3:23])…

etc.…

Observe that the function should expect one argument, which is a vector

of values. rollapply will save the returned values before packaging

them into a zoo object along with a timestamp for every value. The

choice of timestamp depends on the align parameter given to

rollapply:

align="right"The timestamp is taken from the rightmost value.

align="left"The timestamp is taken from the leftmost value.

align="center" (default)The timestamp is taken from the middle value.

By default, rollapply will recalculate the function at successive data

points. You may instead want to calculate the function at every nth

data point. Use the by = n parameter to have rollapply move ahead n

points after each function call. When we calculate the rolling standard

deviation of a time series, for example, we usually want each window of

data to be separate, not overlapping, so we set the by value equal

to the window size:

ibm_sds <- rollapply(ibm_5, width = 30, FUN = sd, by = 30, align = "right")

ibm_sds <- na.omit(ibm_sds)

head(ibm_sds)The rollapply function will, by default, return an object with as many observations as your input data with the missing values filled with NA. In the preceding example we use na.omit to drop the NA values so that our resulting object has records only for the dates for which we have values.

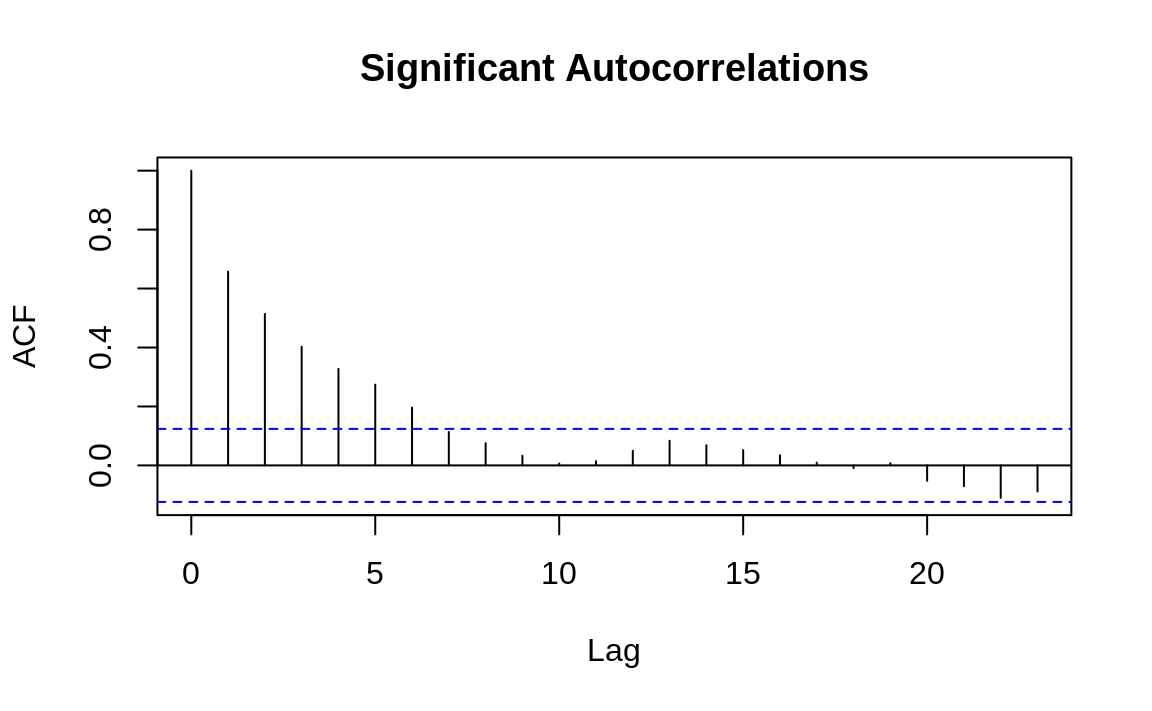

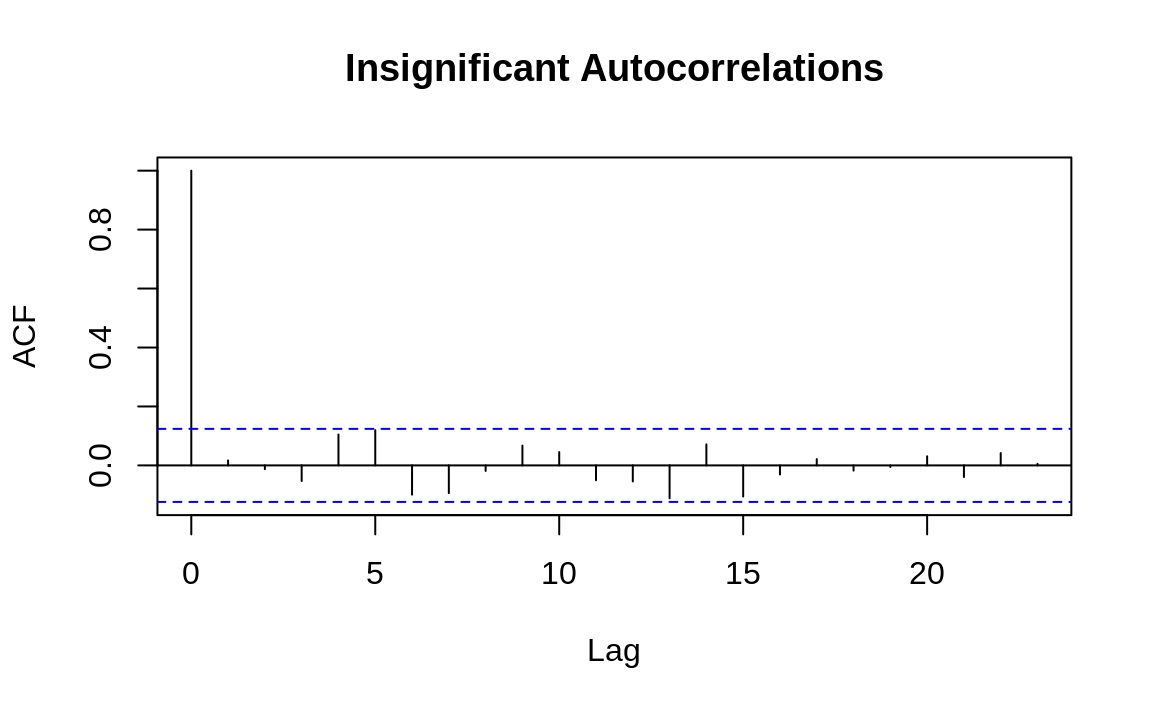

14.13 Plotting the Autocorrelation Function

Problem

You want to plot the autocorrelation function (ACF) of your time series.

Discussion

The autocorrelation function is an important tool for revealing the interrelationships within a time series. It is a collection of correlations, \(\rho_k\) for k = 1, 2, 3, …, where \(\rho_k\) is the correlation between all pairs of data points that are exactly k steps apart.

Visualizing the autocorrelations is much more useful than listing them,

so the acf function plots them for each value of k.

The following example shows the

autocorrelation functions for two time series, one with autocorrelations

and one without. The dashed line delimits the significant and

insignificant correlations: values above the line are significant.

(The height of the dashed line in Figures 14.5 and 14.6 is determined by the amount of data.)

Figure 14.5: Autocorrelations at each lag: ts1

Figure 14.6: Autocorrelations at each lag: ts2

The presence of autocorrelations is one indication that an autoregressive integrated moving average (ARIMA) model could model the time series. From the ACF, you can count the number of significant autocorrelations, which is a useful estimate of the number of moving average (MA) coefficients in the model. Figure 14.5 shows seven significant autocorrelations, for example, so we estimate that its ARIMA model will require seven MA coefficients (MA(7)). That estimate is just a starting point, however, and must be verified by fitting and diagnosing the model.

14.14 Testing a Time Series for Autocorrelation

Problem

You want to test your time series for the presence of autocorrelations.

Solution

Use the Box.test function, which implements the Box–Pierce test for

autocorrelation:

The output includes a p-value. Conventionally, a p-value of less than 0.05 indicates that the data contains significant autocorrelations, whereas a p-value exceeding 0.05 provides no such evidence.

Discussion

Graphing the autocorrelation function is useful for digging into your data. Sometimes, however, we just need to know whether or not the data is autocorrelated. A statistical test such as the Box–Pierce test can provide an answer.

We can apply the Box–Pierce test to the data whose autocorrelation function we plotted in Recipe 14.13, “Plotting the Autocorrelation Function”. The test shows p-values for the two time series that are nearly 0 and 0.79, respectively:

Box.test(ts1)

#>

#> Box-Pierce test

#>

#> data: ts1

#> X-squared = 108, df = 1, p-value <2e-16

Box.test(ts2)

#>

#> Box-Pierce test

#>

#> data: ts2

#> X-squared = 0.07, df = 1, p-value = 0.8The p-value near 0 indicates that the first time series has significant autocorrelations. (We don’t know which autocorrelations are significant; we just know they exist.) The p-value of 0.8 indicates that the test did not detect autocorrelations in the second time series.

The Box.test function can also perform the Ljung–Box test, which is

better for small samples. That test calculates a p-value whose

interpretation is the same as that for the Box–Pierce p-value:

See Also

See Recipe 14.13, “Plotting the Autocorrelation Function”, to plot the autocorrelation function, a visual check of the autocorrelation.

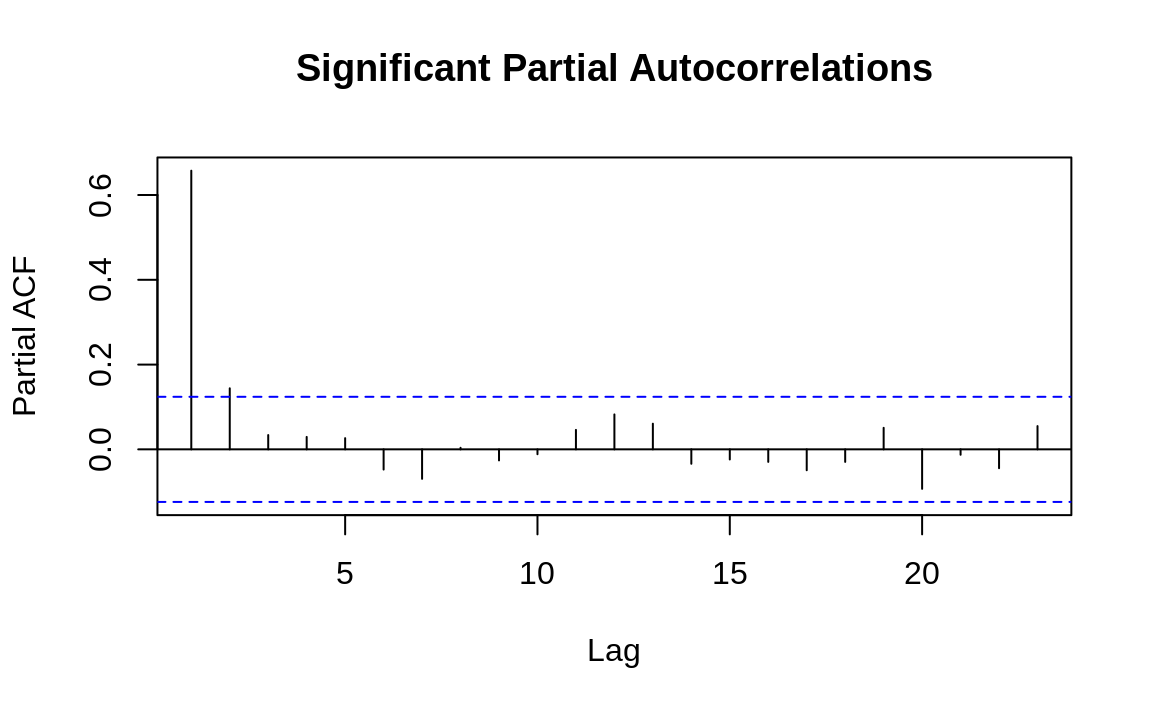

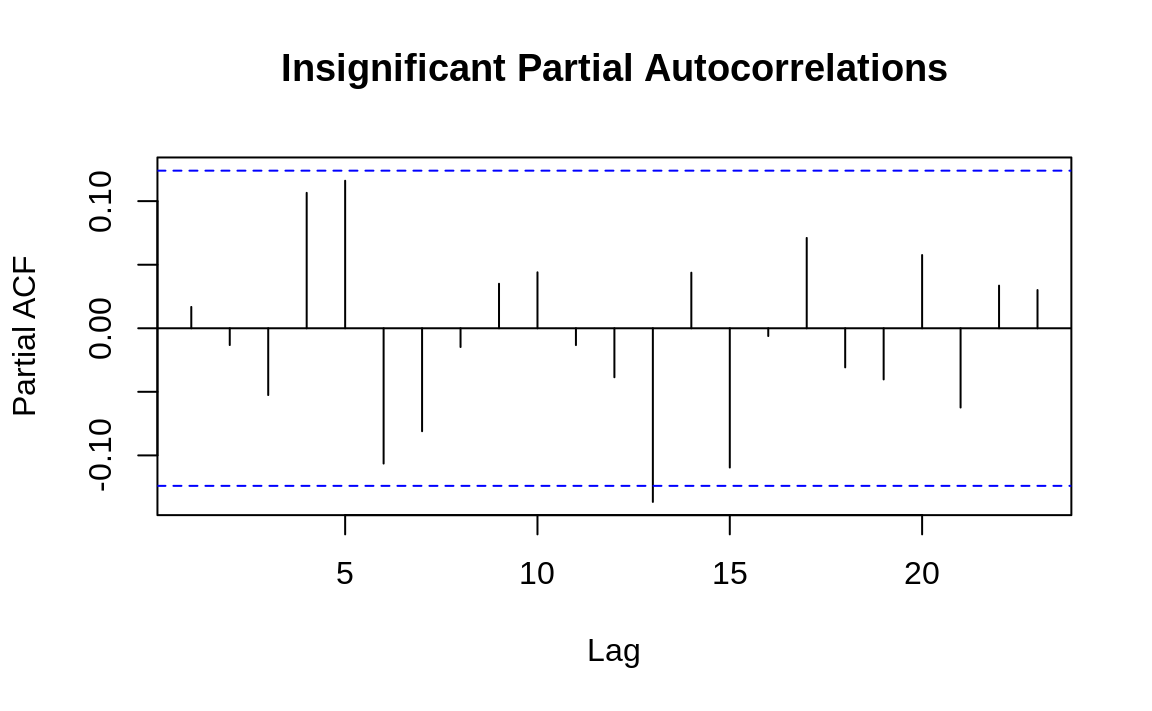

14.15 Plotting the Partial Autocorrelation Function

Problem

You want to plot the partial autocorrelation function (PACF) for your time series.

Discussion

The partial autocorrelation function is another tool for revealing the interrelationships in a time series. However, its interpretation is much less intuitive than that of the autocorrelation function. We’ll leave the mathematical definition of partial correlation to a textbook on statistics. Here, we’ll just say that the partial correlation between two random variables, X and Y, is the correlation that remains after accounting for the correlation shown by X and Y, with all other variables. In the case of time series, the partial autocorrelation at lag k is the correlation between all data points that are exactly k steps apart—after accounting for their correlation with the data between those k steps.

The practical value of a PACF is that it helps you to identify the number of autoregression (AR) coefficients in an ARIMA model. The following example shows the PACF for the two time series used in Recipe 14.13, “Plotting the Autocorrelation Function”. One of these series has partial autocorrelations and one does not. Lag values whose lines cross above the dotted line are statistically significant. In the first time series (Figure 14.7) there are two such values, at k = 1 and k = 2, so our initial ARIMA model will have two AR coefficients (AR(2)). As with autocorrelation, however, that is just an initial estimate and must verified by fitting and diagnosing the model. The second time series (Figure 14.8) shows no such autocorrelation pattern.

Figure 14.7: Autocorrelations at each lag: ts1

Figure 14.8: Autocorrelations at each lag: ts2

See Also

See Recipe 14.13, “Plotting the Autocorrelation Function”.

14.16 Finding Lagged Correlations Between Two Time Series

Problem

You have two time series, and you are wondering if there is a lagged correlation between them.

Solution

Use the Ccf function from the package forecast to plot the cross-correlation function, which

will reveal lagged correlations:

Discussion

The cross-correlation function helps you discover lagged correlations between two time series. A lagged correlation occurs when today’s value in one time series is correlated with a future or past value in the other time series.

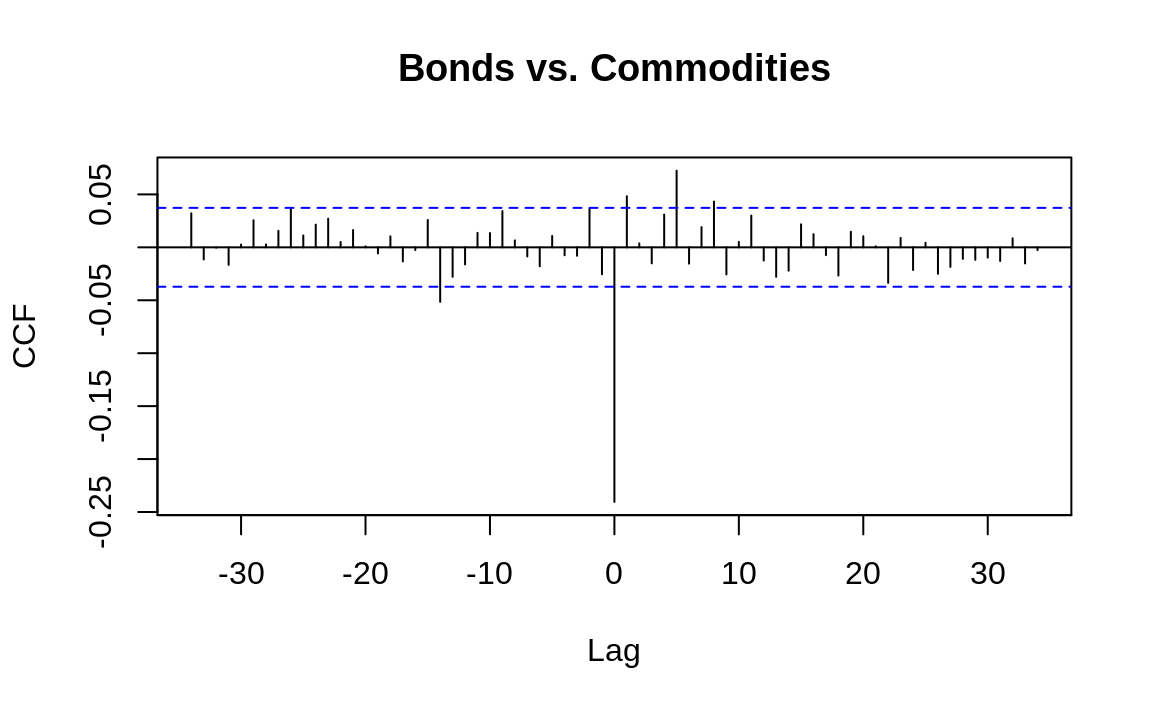

Consider the relationship between commodity prices and bond prices. Some analysts believe those prices are connected because changes in commodity prices are a barometer of inflation, one of the key factors in bond pricing. Can we discover a correlation between them?

Figure 14.9 shows a cross-correlation function generated from daily changes in bond prices and a commodity price index:5

library(forecast)

#> Registered S3 method overwritten by 'quantmod':

#> method from

#> as.zoo.data.frame zoo

#> Registered S3 methods overwritten by 'forecast':

#> method from

#> fitted.fracdiff fracdiff

#> residuals.fracdiff fracdiff

load(file = "./data/bnd_cmty.Rdata")

b <- coredata(bonds)[, 1]

c <- coredata(cmdtys)[, 1]

Ccf(b, c, main = "Bonds vs. Commodities")

Figure 14.9: Cross-correlation function

Note that since the objects we start with, bonds and cmdtys, are xts objects, we extract from each the vector of data using coredata()[1]. This is because the Ccf function expects inputs to be simple vectors.

Every vertical line shows the correlation between the two time series at some lag, as indicated along the x-axis. If a correlation extends above or below the dotted lines, it is statistically significant.

Notice that the correlation at lag 0 is –0.24, which is the simple correlation between the variables:

Much more interesting are the correlations at lags 1, 5, and 8, which are statistically significant. Evidently there is some “ripple effect” in the day-to-day prices of bonds and commodities because changes today are correlated with changes tomorrow. Discovering this sort of relationship is useful to short-term forecasters such as market analysts and bond traders.

14.17 Detrending a Time Series

Problem

Your time series data contains a trend that you want to remove.

Solution

Use linear regression to identify the trend component, and then subtract the

trend component from the original time series. These two lines show how

to detrend the zoo object ts and put the result in detr:

Discussion

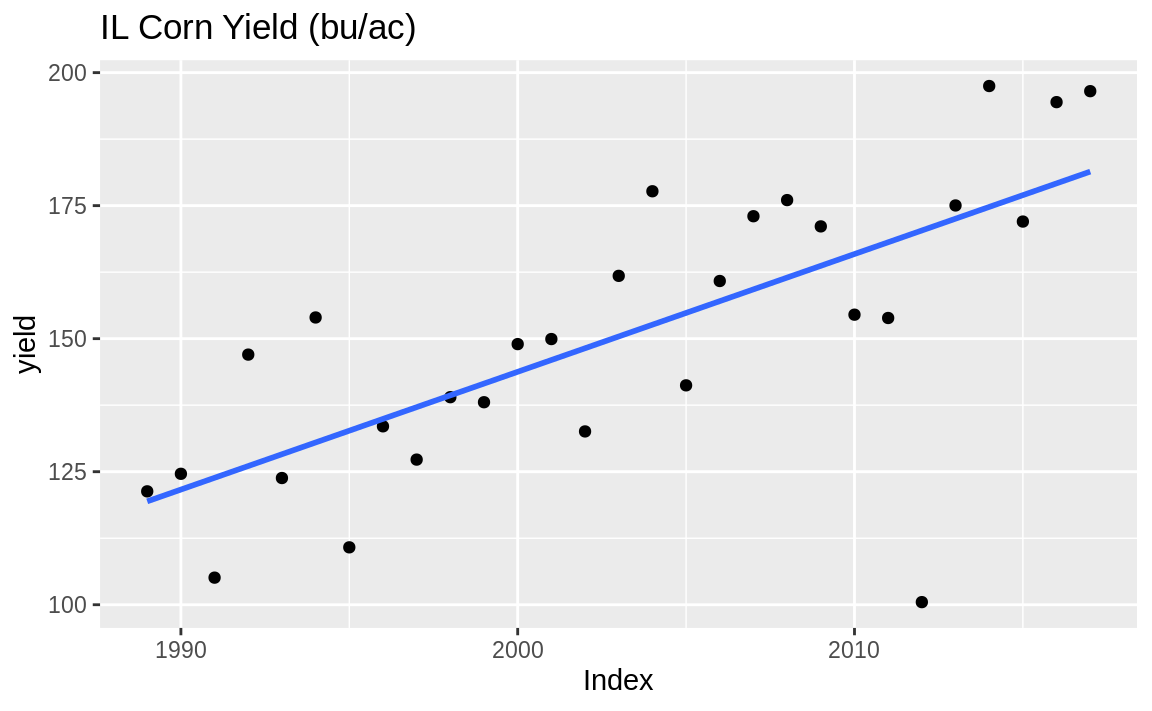

Some time series data contains trends, which means that it gradually

slopes upward or downward over time. Suppose your time series object (a zoo object in this case), yield, contains a trend as shown in Figure 14.10:

Figure 14.10: Time series with trend

We can remove the trend component in two steps. First, identify the

overall trend by using the linear model function, lm. The model should

use the time series index for the x variable and the time series data

for the y variable.

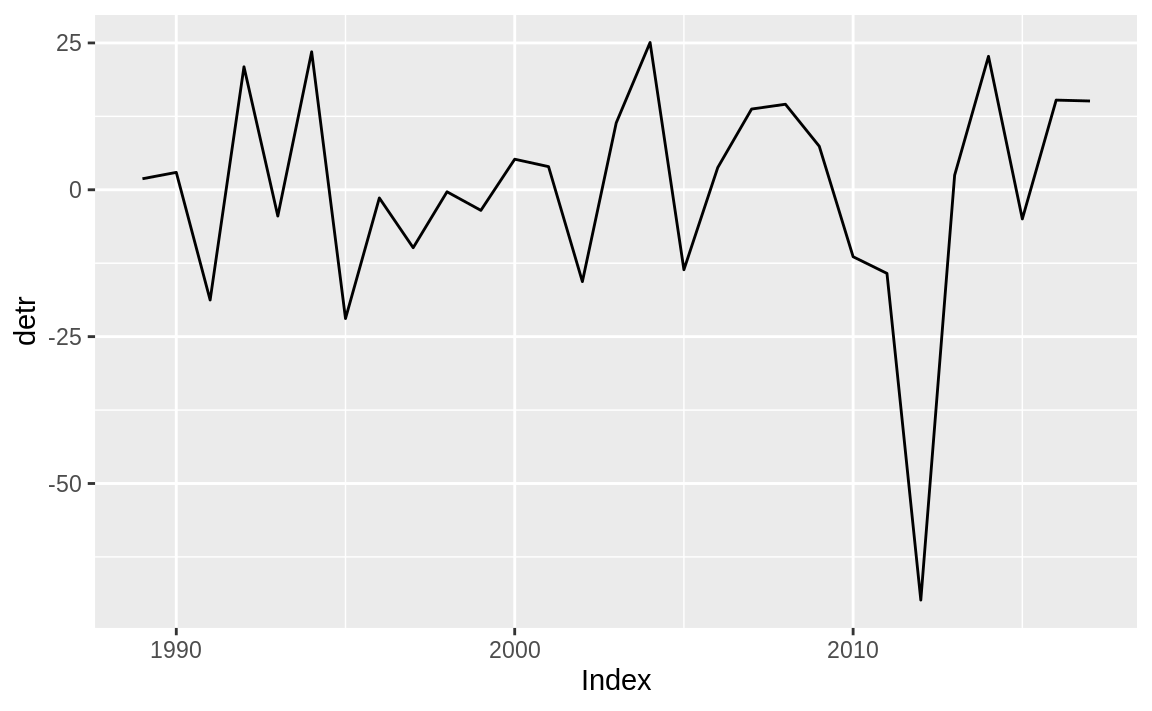

Second, remove the linear trend from the original data by subtracting

the straight line found by lm. This is easy because we have access to

the linear model’s residuals, which are defined by the difference

between the original data and the fitted line:

\(r_i = y_i - \beta_1 x_i - \beta_0\)

where \(r_i\) is the ith residual, and where \(\beta_1\) and \(\beta_0\) are the

model’s slope and intercept, respectively. We can extract the residuals

from the linear model by using the resid function and then embed the

residuals inside a zoo object:

Notice that we use the same time index as the original data. When we

plot detr it is clearly trendless, as evident in Figure 14.11.

Figure 14.11: Residual plot

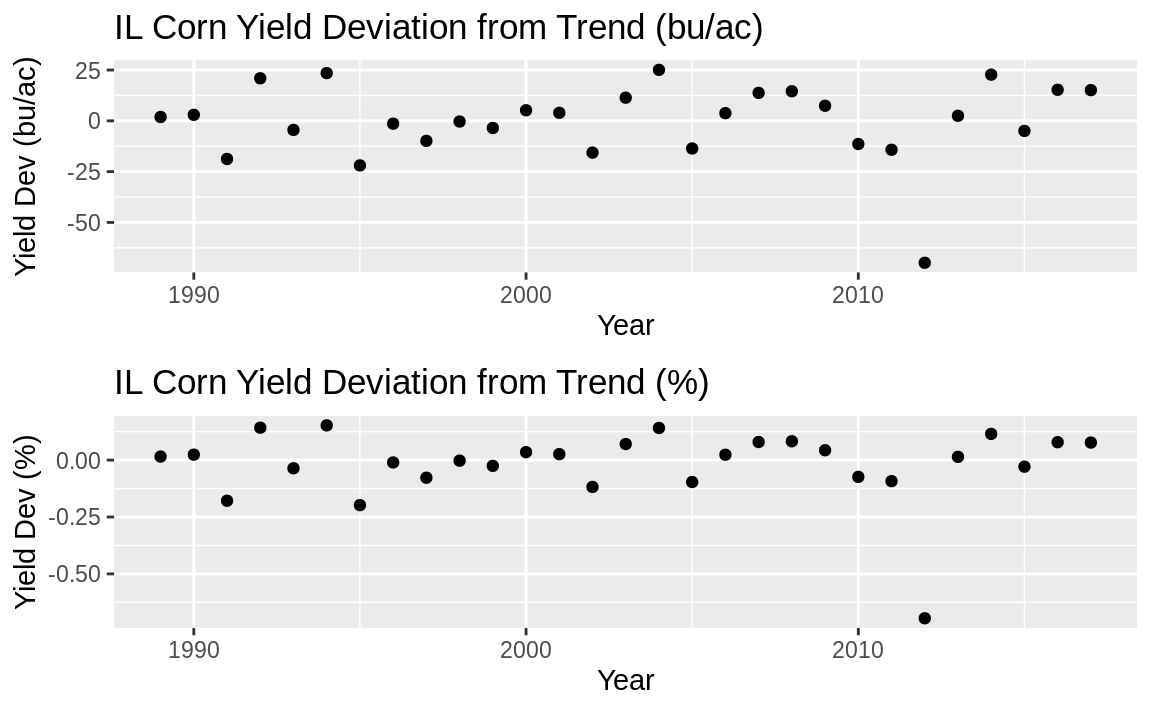

This data is the state average corn yield for Illinois in bushels per acre (bu/ac). So detr is the difference between actual yield and the trend. Sometimes when detrending you may want to determine the percent deviation from the trend. In that case we can divide by the initial measure:

library(patchwork)

# y <- autoplot(yield) +

# labs(x='Year', y='Yield (bu/ac)', title='IL Corn Yield')

d <- autoplot(detr, geom = "point") +

labs(

x = "Year", y = "Yield Dev (bu/ac)",

title = "IL Corn Yield Deviation from Trend (bu/ac)"

)

dp <- autoplot(detr / yield, geom = "point") +

labs(

x = "Year", y = "Yield Dev (%)",

title = "IL Corn Yield Deviation from Trend (%)"

)

d / dp

Figure 14.12: Detrended plots

The top plot in Figure 14.12 shows the yield deviation from the trend in bu/ac (the original units), while the lower plot shows the percent deviation from the trend.

14.18 Fitting an ARIMA Model

Problem

You want to fit an ARIMA model to your time series data.

Solution

The auto.arima function in the forecast package can select the

correct model order and fit the model to your data:

If you already know the model order, (p, d, q), then the arima

function can fit the model directly:

Discussion

Creating an ARIMA model involves three steps:

Identify the model order.

Fit the model to the data, giving the coefficients.

Apply diagnostic measures to validate the model.

The model order is usually denoted by three integers, (p, d, q), where p is the number of autoregressive coefficients, d is the degree of differencing, and q is the number of moving average coefficients.

When most of us build an ARIMA model, we are usually clueless about the appropriate

order. Rather than tediously searching for the best combination of p,

d, and q, we typically use auto.arima, which does the searching for us:

library(forecast)

library(fpp2) # for example data

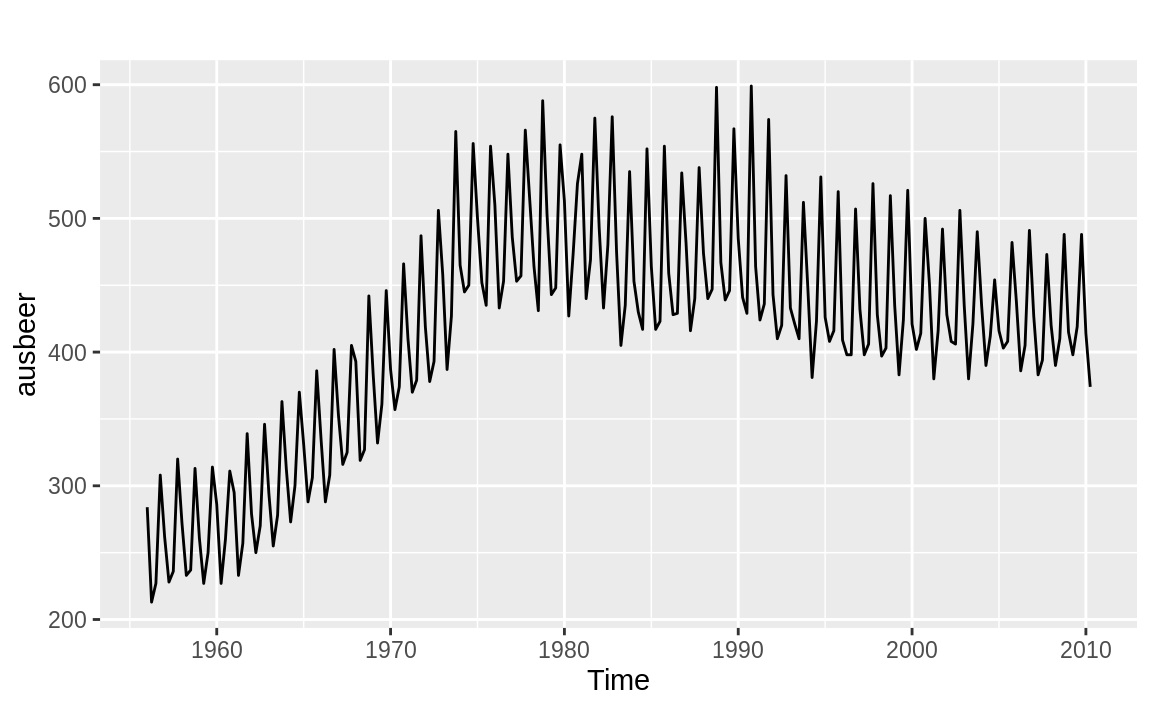

auto.arima(ausbeer)

#> Series: ausbeer

#> ARIMA(1,1,2)(0,1,1)[4]

#>

#> Coefficients:

#> ar1 ma1 ma2 sma1

#> 0.050 -1.009 0.375 -0.743

#> s.e. 0.196 0.183 0.153 0.050

#>

#> sigma^2 estimated as 241: log likelihood=-886

#> AIC=1783 AICc=1783 BIC=1800In this case, auto.arima decided the best order was (1, 1, 2), which

means that it differenced the data once (d = 1) before selecting a

model with AR coefficients (p = 1) and two MA coefficients (q =

2). In addition, the auto.arima function determined that our data has seasonality and included the seasonal terms P = 0, D = 1, Q = 1 and a period of m = 4. The seasonality terms are similar to the nonseasonal ARIMA terms, but relate to the seasonality component of the model. The m term tells us the periodicity of the seasonality, which in this case is quarterly. We can see this easier if we plot the ausbeer data as in Figure 14.13:

Figure 14.13: Australian beer consumption

By default, auto.arima limits p and q to the range 0 ≤ p ≤ 5 and

0 ≤ q ≤ 5. If you are confident that your model needs fewer than five

coefficients, use the max.p and max.q parameters to limit the search

further; this makes it faster. Likewise, if you believe that your model

needs more coefficients, use max.p and max.q to expand the search

limits.

If you want to turn off the seasonality component of auto.arima, you can set seasonal = FALSE:

auto.arima(ausbeer, seasonal = FALSE)

#> Series: ausbeer

#> ARIMA(3,2,2)

#>

#> Coefficients:

#> ar1 ar2 ar3 ma1 ma2

#> -0.957 -0.987 -0.925 -1.043 0.142

#> s.e. 0.026 0.018 0.024 0.062 0.062

#>

#> sigma^2 estimated as 327: log likelihood=-935

#> AIC=1882 AICc=1882 BIC=1902But notice that since the model fits a nonseasonal model, the coefficients are different than in the seasonal model.

If you already know the order of your ARIMA model, the arima function

can quickly fit the model to your data:

arima(ausbeer, order = c(3, 2, 2))

#>

#> Call:

#> arima(x = ausbeer, order = c(3, 2, 2))

#>

#> Coefficients:

#> ar1 ar2 ar3 ma1 ma2

#> -0.957 -0.987 -0.925 -1.043 0.142

#> s.e. 0.026 0.018 0.024 0.062 0.062

#>

#> sigma^2 estimated as 319: log likelihood = -935, aic = 1882The output looks identical to auto.arima with the seasonal parameter set to FALSE. What you can’t see here is that arima executes much more quickly.

The output from auto.arima and arima includes the fitted

coefficients and the standard error (s.e.) for each coefficient:

Coefficients:

ar1 ar2 ar3 ma1 ma2

-0.9569 -0.9872 -0.9247 -1.0425 0.1416

s.e. 0.0257 0.0184 0.0242 0.0619 0.0623You can find the coefficients’ confidence intervals by capturing the

ARIMA model in an object and then using the confint function:

m <- arima(x = ausbeer, order = c(3, 2, 2))

confint(m)

#> 2.5 % 97.5 %

#> ar1 -1.0072 -0.907

#> ar2 -1.0232 -0.951

#> ar3 -0.9721 -0.877

#> ma1 -1.1639 -0.921

#> ma2 0.0195 0.264This output illustrates a major headache of ARIMA modeling: not all the coefficients are necessarily significant. If one of the intervals contains zero, the true coefficient might be zero itself, in which case the term is unnecessary.

If you discover that your model contains insignificant coefficients, use Recipe 14.19, “Removing Insignificant ARIMA Coefficients”, to remove them.

The auto.arima and arima functions contain useful features for

fitting the best model. For example, you can force them to include or

exclude a trend component. See the help pages for details.

A final caveat: the danger of auto.arima is that it makes ARIMA

modeling look simple. ARIMA modeling is not simple. It is more art

than science, and the automatically generated model is just a starting

point. We urge you to review a good book about ARIMA modeling

before settling on a final model.

See Also

See Recipe 14.20, “Running Diagnostics on an ARIMA Model”, for performing diagnostic tests on the ARIMA model.

As a textbook on time series forecasting, we highly recommend Forecasting: Principles and Practice by Rob J. Hyndman and George Athanasopoulos which is freely available online.

14.19 Removing Insignificant ARIMA Coefficients

Problem

One or more of the coefficients in your ARIMA model are statistically insignificant. You want to remove them.

Solution

The arima function includes the parameter fixed, which is a vector.

The vector should contain one element for every coefficient in the

model, including a term for the drift (if any). Each element is either

NA or 0. Use NA for the coefficients to be kept and use 0 for the

coefficients to be removed. This example shows an ARIMA(2, 1, 2) model

with the first AR coefficient and the first MA coefficient forced to be

0:

Discussion

The fpp2 package contains a dataset called euretail, which is a quarterly retail index for the Euro area. Let’s run auto.arima on the data and look at the 98% confidence intervals:

m <- auto.arima(euretail)

m

#> Series: euretail

#> ARIMA(0,1,3)(0,1,1)[4]

#>

#> Coefficients:

#> ma1 ma2 ma3 sma1

#> 0.263 0.369 0.420 -0.664

#> s.e. 0.124 0.126 0.129 0.155

#>

#> sigma^2 estimated as 0.156: log likelihood=-28.6

#> AIC=67.3 AICc=68.4 BIC=77.7

confint(m, level = .98)

#> 1 % 99 %

#> ma1 -0.0246 0.551

#> ma2 0.0774 0.661

#> ma3 0.1190 0.721

#> sma1 -1.0231 -0.304In this example, we can see that the 98% confidence interval for the ma1 parameter contains 0 and we can reasonably conclude that this parameter is insignificant at this level of confidence. We can set this parameter to 0 using the fixed parameter:

m <- arima(euretail, order = c(0, 1, 3), seasonal = c(0, 1, 1), fixed = c(0, NA, NA, NA))

m

#>

#> Call:

#> arima(x = euretail, order = c(0, 1, 3), seasonal = c(0, 1, 1), fixed = c(0,

#> NA, NA, NA))

#>

#> Coefficients:

#> ma1 ma2 ma3 sma1

#> 0 0.404 0.293 -0.700

#> s.e. 0 0.129 0.107 0.135

#>

#> sigma^2 estimated as 0.156: log likelihood = -30.8, aic = 69.5Observe that the ma1 coefficient is now 0. The

remaining coefficients (ma2, ma3, sma1) are still significant, as shown

by their confidence intervals, so we have a reasonable model:

14.20 Running Diagnostics on an ARIMA Model

Problem

You have built an ARIMA model using the forecast package, and you want to run diagnostic tests to

validate the model.

Solution

Use the checkresiduals function. This example fits the ARIMA model using auto.arima, puts the results in m, and then runs diagnostics on the model:

Discussion

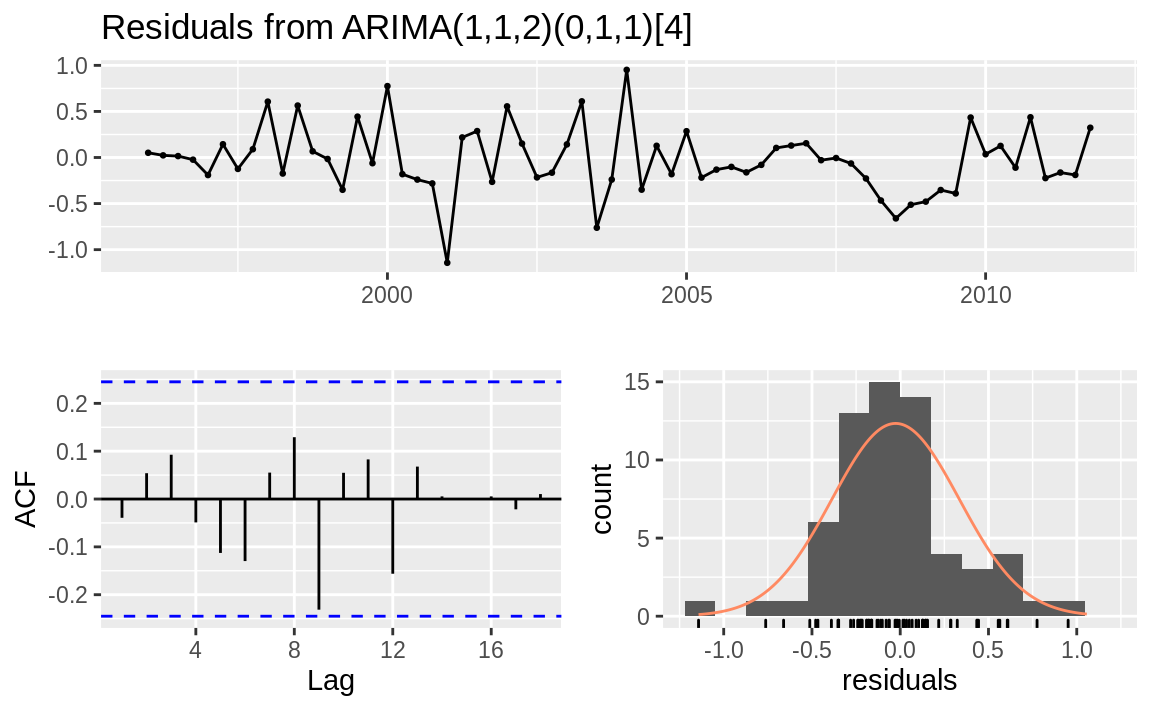

The result of checkresiduals is a set of three graphs, as shown in Figure 14.14. A good model should

produce results like these:

#>

#> Ljung-Box test

#>

#> data: Residuals from ARIMA(1,1,2)(0,1,1)[4]

#> Q* = 5, df = 4, p-value = 0.3

#>

#> Model df: 4. Total lags used: 8

Figure 14.14: Residuals plots: Good model

Here’s what’s good about the graphs:

The standardized residuals don’t show clusters of volatility.

The autocorrelation function (ACF) shows no significant autocorrelation between the residuals.

The residuals look bell-shaped, suggesting they are reasonably symmetrical.

The p-value in the Ljung–Box test is large, indicating that the residuals are patternless—meaning all the information has been extracted by the model and only noise is left behind.

For contrast, Figure 14.15 shows diagnostic charts with problems:

#>

#> Ljung-Box test

#>

#> data: Residuals from ARIMA(1,1,1)(0,0,1)[4]

#> Q* = 22, df = 5, p-value = 5e-04

#>

#> Model df: 3. Total lags used: 8

Figure 14.15: Residuals plots: Problem model

The ACF shows significant autocorrelations between residuals.

The p-values for the Ljung–Box statistics are small, indicating there is some pattern in the residuals. There is still information to be extracted from the data.

The residuals appear asymmetrical.

These are basic diagnostics, but they are a good start. Find a good book on ARIMA modeling and perform the recommended diagnostic tests before concluding that your model is sound. Additional checks of the residuals could include:

- Tests for normality

- Quantile–quantile (Q–Q) plot

- Scatter plot against the fitted values

14.21 Making Forecasts from an ARIMA Model

Problem

You have an ARIMA model for your time series that you built with the forecast package. You want to forecast the

next few observations in the series.

Solution

Save the model in an object, and then apply the forecast function to the

object. This example saves the model from Recipe 14.19, “Removing Insignificant ARIMA Coefficients”, and predicts

the next eight observations:

m <- arima(euretail, order = c(0, 1, 3), seasonal = c(0, 1, 1), fixed = c(0, NA, NA, NA))

forecast(m)

#> Point Forecast Lo 80 Hi 80 Lo 95 Hi 95

#> 2012 Q1 95.1 94.6 95.6 94.3 95.9

#> 2012 Q2 95.2 94.5 95.9 94.1 96.3

#> 2012 Q3 95.2 94.2 96.3 93.7 96.8

#> 2012 Q4 95.3 93.9 96.6 93.2 97.3

#> 2013 Q1 94.5 92.8 96.1 91.9 97.0

#> 2013 Q2 94.5 92.6 96.5 91.5 97.5

#> 2013 Q3 94.5 92.3 96.7 91.1 97.9

#> 2013 Q4 94.5 92.0 97.0 90.7 98.3Discussion

The forecast function will calculate the next few observations and their

standard errors according to the model. It returns a list with 10

elements. When we print the model, as we just did, forecast returns the time series points it is forecasting, the forecast, and two pairs of confidence bands: high/low 80% and high/low 95%.

If we want to extract out just the forecast, we can do that by assigning the results to an object, and then pulling out the list item named mean:

fc_m <- forecast(m)

fc_m$mean

#> Qtr1 Qtr2 Qtr3 Qtr4

#> 2012 95.1 95.2 95.2 95.3

#> 2013 94.5 94.5 94.5 94.5The result is a Time-Series object containing the forecasts created by the forecast function.

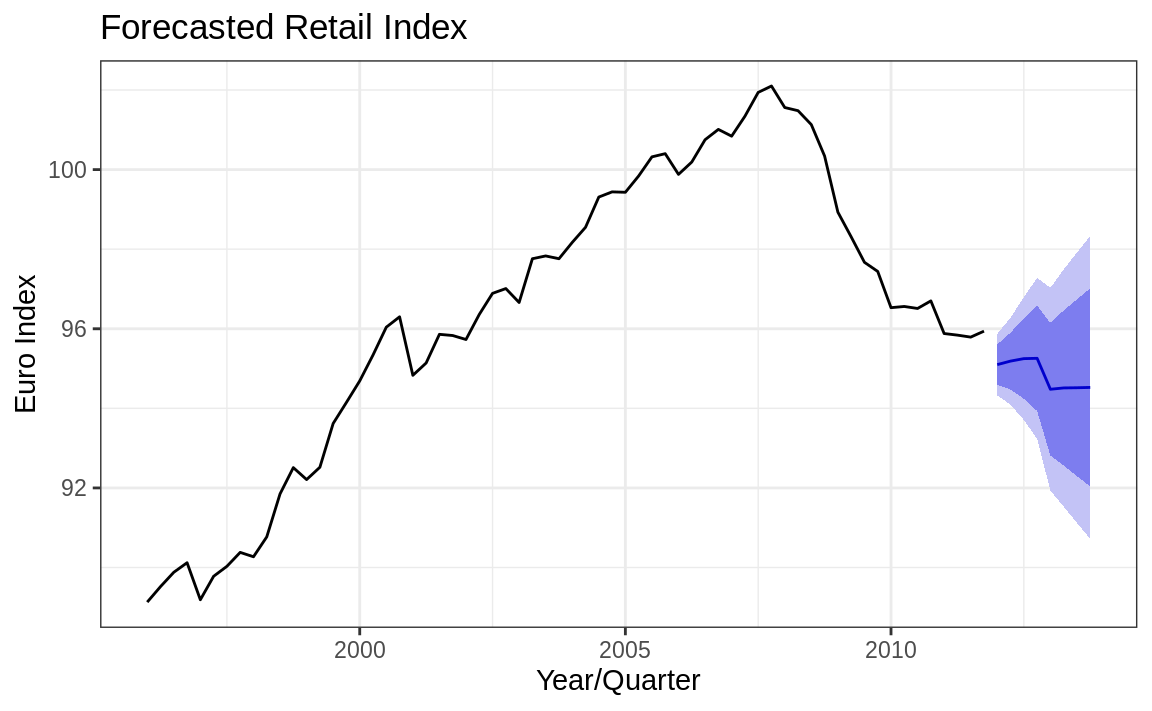

14.22 Plotting a Forecast

Problem

You have created a time series forecast with the forecast package and you would like to plot it.

Solution

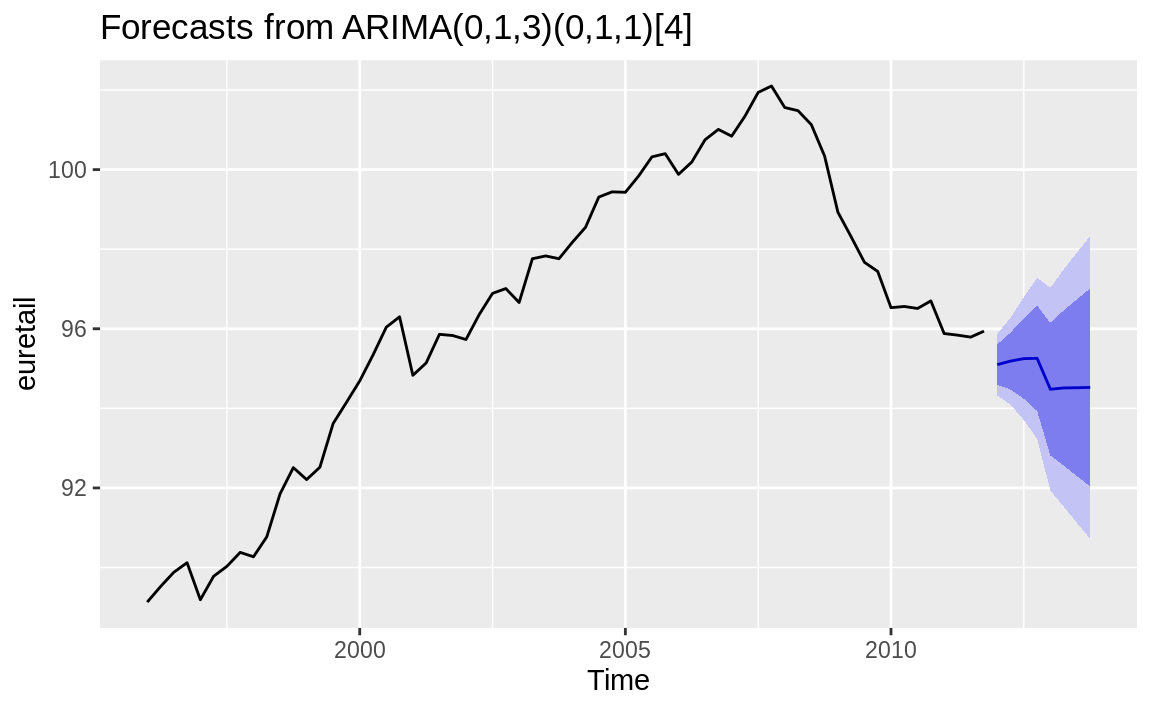

Time series models created with the forecast package have a plotting method that uses ggplot2 to create graphs easily, as shown in Figure 14.16:

Figure 14.16: Forecast cone of uncertainty: Default

Discussion

The autoplot function makes a very reasonable figure, as shown in Figure 14.16. Since the resulting figure is a ggplot object, we can adjust the plotting parameters the same way we would any other ggplot object. Here we add labels and a title and change the theme, as shown in Figure 14.17:

autoplot(fc_m) +

ylab("Euro Index") +

xlab("Year/Quarter") +

ggtitle("Forecasted Retail Index") +

theme_bw()

Figure 14.17: Forecast cone of uncertainty: Labeled

See Also

Chapter @ref(#Graphics) for more info on working with ggplot figures.

14.23 Testing for Mean Reversion

Problem

You want to know if your time series is mean reverting (stationary).

Solution

A common test for mean reversion is the Augmented Dickey–Fuller (ADF)

test, which is implemented by the adf.test function of the tseries

package:

The output from adf.test includes a p-value. Conventionally, if p

< 0.05, the time series is likely mean reverting, whereas a p

> 0.05 provides no such evidence.

Discussion

When a time series is mean reverting, it tends to return to its long-run average. It may wander off, but eventually it wanders back. If a time series is not mean reverting, then it can wander away without ever returning to the mean.

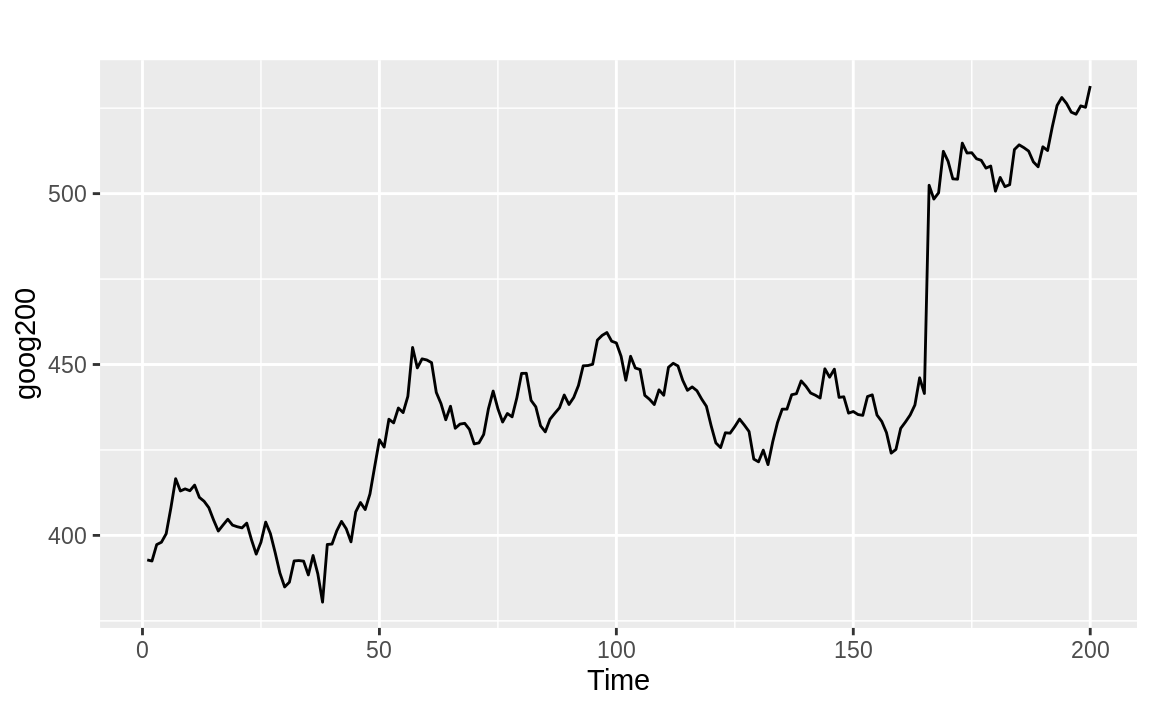

Figure 14.18 appears to be wandering upward and not returning. The large p-value from the adf.test confirms that it is not mean reverting:

library(tseries)

library(fpp2)

autoplot(goog200)

adf.test(goog200)

#>

#> Augmented Dickey-Fuller Test

#>

#> data: goog200

#> Dickey-Fuller = -2, Lag order = 5, p-value = 0.7

#> alternative hypothesis: stationary

Figure 14.18: Time series without mean reversion

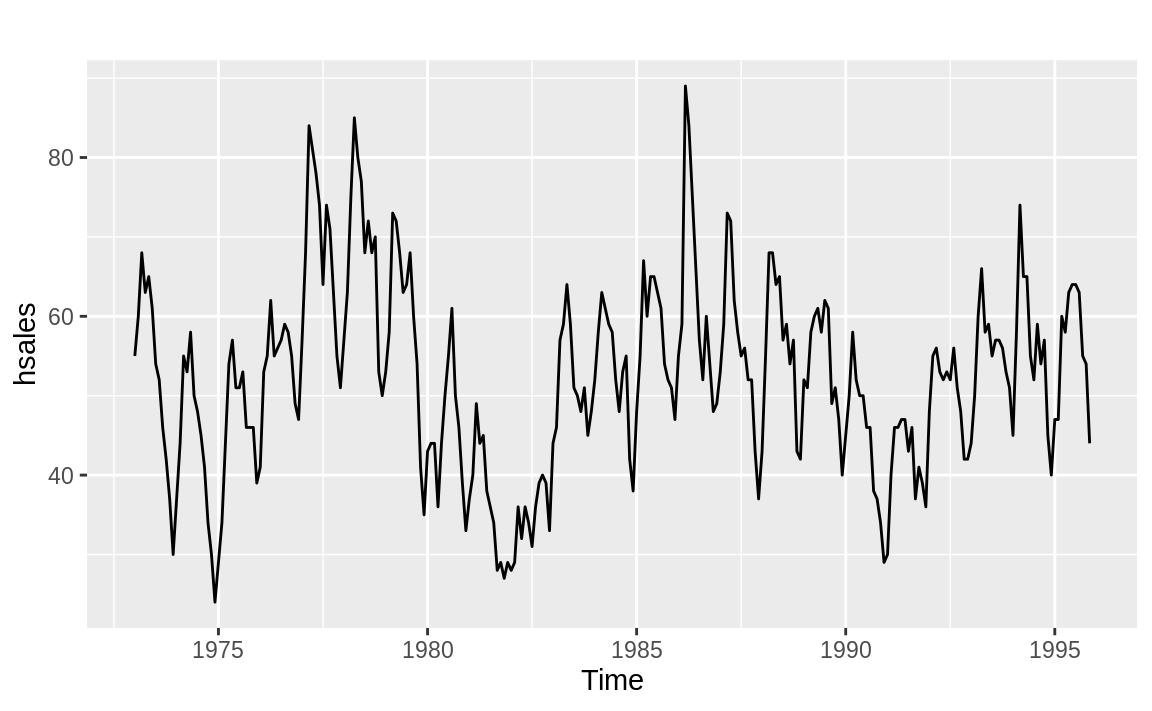

The time series in Figure 14.19, however, is just bouncing around its average value. The small p-value (0.012) confirms that it is mean reverting:

autoplot(hsales)

adf.test(hsales)

#>

#> Augmented Dickey-Fuller Test

#>

#> data: hsales

#> Dickey-Fuller = -4, Lag order = 6, p-value = 0.01

#> alternative hypothesis: stationary

Figure 14.19: Time series with mean reversion

The example data here comes from the fpp2 package and comprises all Time-Series object types.

If your data were in a zoo or xts object, then you would need to call coredata to extract out the raw data from the object before passing it to adf.test:

library(xts)

data(sample_matrix)

xts_obj <- as.xts(sample_matrix, dateFormat = "Date")[, "Close"] # single vector of data

adf.test(coredata(xts_obj))

#>

#> Augmented Dickey-Fuller Test

#>

#> data: coredata(xts_obj)

#> Dickey-Fuller = -3, Lag order = 5, p-value = 0.3

#> alternative hypothesis: stationaryThe adf.test function massages your data before performing the ADF

test. First it automatically detrends your data, and then it recenters the

data, giving it a mean of 0.

If either detrending or recentering is undesirable for your application,

use the adfTest function in the fUnitRoots package instead:

With type = "nc", the function neither detrends nor recenters your data.

With type = "c", the function recenters your data but does not detrend

it.

Both the adf.test and the adfTest functions let you specify a lag

value that controls the exact statistic they calculate. These functions

provide reasonable defaults, but serious users should study the

textbook description of the ADF test to determine the appropriate lag

for their application.

See Also

The urca and CADFtest packages also implement tests for a unit root,

which is the test for mean reversion. Be careful when comparing the

tests from several packages. Each package can make slightly different

assumptions, which can lead to puzzling differences in the results.

14.24 Smoothing a Time Series

Problem

You have a noisy time series. You want to smooth the data to eliminate the noise.

Solution

The KernSmooth package contains functions for smoothing. Use the

dpill function to select an initial bandwidth parameter, and then use the

locploy function to smooth the data:

library(KernSmooth)

gridsize <- length(y)

bw <- dpill(t, y, gridsize = gridsize)

lp <- locpoly(x = t, y = y, bandwidth = bw, gridsize = gridsize)

smooth <- lp$yHere, t is the time variable and y is the time series.

Discussion

The KernSmooth package is a standard part of the R distribution. It

includes the locpoly function, which constructs, around each

data point, a polynomial that is fitted to the nearby data points.

These are called local polynomials. The local polynomials are strung

together to create a smoothed version of the original data series.

The algorithm requires a bandwidth parameter to control the degree of smoothing. A small bandwidth means less smoothing, in which case the result follows the original data more closely. A large bandwidth means more smoothing, so the result contains less noise. The tricky part is choosing just the right bandwidth: not too small, not too large.

Fortunately, KernSmooth also includes the function dpill for

estimating the appropriate bandwidth, and it works quite well.

We recommend that you start with the dpill value and then experiment with

values above and below that starting point. There is no magic formula

here. You need to decide what level of smoothing works best in your

application.

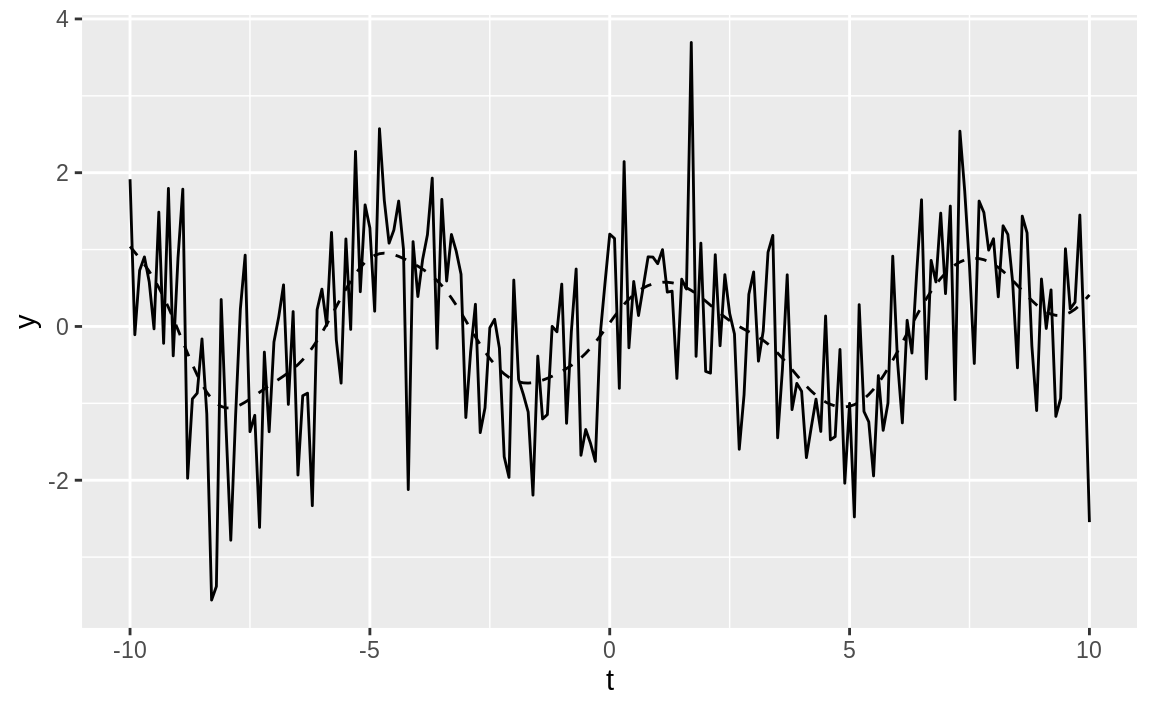

The following is an example of smoothing. We’ll create some example data that is the sum of a simple sine wave and normally distributed “noise”:

Both dpill and locpoly require a grid size—in other words, the number of

points for which a local polynomial is constructed.

We often use a grid size equal to the number of data points, which yields a fine resolution.

The resulting time series is very smooth. You might use a smaller grid

size if you want a coarser resolution or if you have a very large

dataset:

The locpoly function performs the smoothing and returns a list. The

y element of that list is the smoothed data:

lp <- locpoly(x = t, y = y, bandwidth = bw, gridsize = gridsize)

smooth <- lp$y

ggplot() +

geom_line(aes(x = t, y = y)) +

geom_line(aes(x = t, y = smooth), linetype = 2)

Figure 14.20: Example time series plot

In Figure 14.20, the smoothed data is shown

as a dashed line, while the solid line is our original example data. The figure demonstrates that locpoly did an

excellent job of extracting the original sine wave.

See Also

The ksmooth, lowess, and HoltWinters functions in the base

distribution can also perform smoothing. The expsmooth package

implements exponential smoothing.

Specifically: the

bondsvariable is the log-returns of the Vanguard Long-Term Bond Index Fund (VBLTX), and thecmdtysvariable is the log-returns of the Invesco DB Commodity Tracking Fund (DBC). The data was taken from the period 2007-01-01 through 2017-12-31.↩